The $500,000 Mistake: Why Sitting on Your Divorce Will Cost You Everything You Earned

The Financial Advisor Who Could Lose Half of Everything Built Alone

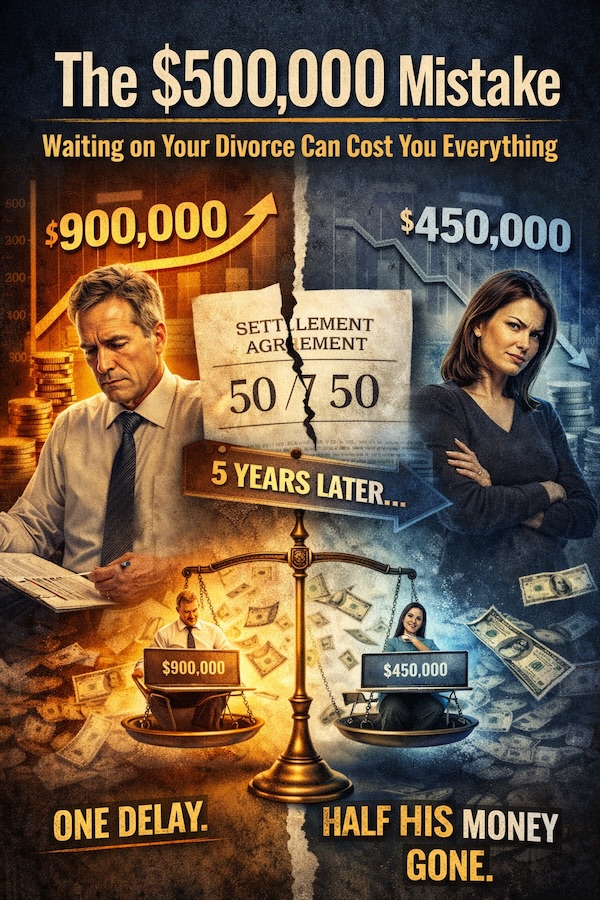

Picture this hypothetical scenario: You’re a financial advisor going through a divorce. At the time you separate from your spouse, you each have approximately $400,000 in investment accounts. Your spouse tells you they don’t want you managing their money anymore. You say fine, and you each go your separate ways financially.

Five years pass. Your ex-spouse does nothing with the divorce case. You don’t push it either—you’re busy, they seem fine with the status quo, and honestly, it’s easier to just let things sit.

During those five years, you do what you do best: you manage investments. Your $400,000 grows to $900,000—more than doubling your initial portfolio. Meanwhile, your ex-spouse’s $400,000 grows to only $450,000. They gained just $50,000 while you gained $500,000.

When you finally get to divorce settlement, you expect to keep your $900,000, right? After all, you’ve been separated for five years. You built that $500,000 increase through your own skill and effort after the marriage ended.

This assumption could cost you $250,000.

The Brutal Reality of Community Property During Separation

Here’s what California law requires in this scenario: you would have to give your ex-spouse half of that $900,000.

That’s right—even though you alone built the account from $400,000 to $900,000 over five years of separation, the entire $900,000 could remain community property. You would walk away with $450,000. They would walk away with $450,000.

They would essentially receive half of the $500,000 you earned through your own efforts during five years of separation—while you would only receive $25,000 of their $50,000 gain.

How is this possible? How can money you earn after separation still belong to your spouse?

Why Separated Doesn’t Mean Separate Property

Here’s the critical concept many people don’t understand: separation date and community property are two different things.

Yes, the date of separation is legally significant. It determines when you stop accumulating new community property and when your earnings become your separate property.

But—and this is crucial—assets that were already community property at the time of separation remain community property until your divorce is finalized.

In our hypothetical scenario:

- The $400,000 investment account existed during the marriage

- It was acquired and built during the marriage

- It was 100% community property

- When separation occurred, it remained 100% community property

- The characterization of the asset didn’t change just because of separation

Even though five years might pass after separation, even though one spouse exclusively manages the account, even though the other spouse has no involvement whatsoever, the account remains community property. And community property must be divided equally.

The Fiduciary Duty That Could Cost You $250,000

Here’s what makes this even more painful: because you would be managing a community property asset, you have a legal fiduciary duty to grow it, protect it, and manage it responsibly.

If you take the account from $400,000 to $900,000—exceptional performance by any measure—you’ve done exactly what the law requires.

But that fiduciary duty means you’re managing the asset for the community, not just for yourself. Your skill, your time, your expertise all benefit the community property. The law treats your management as a community contribution, which means the growth belongs equally to both spouses.

Meanwhile, if your ex-spouse’s account barely grows under their management, they still get to keep their entire portion and take half of yours.

The unfairness is obvious. But it’s perfectly legal under California community property law.

The Delay That Changes Everything

The devastating part of this hypothetical is that it would be completely avoidable.

Imagine a spouse files for divorce, serves the papers, and then… nothing. The case sits dormant for years. They have no intention of moving forward. They’re content being separated, living apart, and just leaving the legal status unchanged.

If the other spouse doesn’t push either, waiting years before even hiring an attorney, the financial damage accumulates with each passing month.

If someone hired an attorney immediately and pushed for quick resolution, the story would be very different:

- The $400,000 would be divided when it was still $400,000

- Each spouse would receive $200,000 as their share

- Everything earned after that would be separate property

- A separate account could grow from $200,000 to potentially $450,000 or more—all kept by whoever earned it

- Each spouse would be responsible for their own growth

Instead, someone could lose approximately $250,000 by waiting.

The Dangers of the “Friendly” Divorce

Sometimes in a divorce, one spouse has zero motivation to finalize things. They’ve moved out, established their own life, and are perfectly fine letting things stay in legal limbo.

Their attorney might be just as unresponsive and uncooperative as they are. Throughout potential litigation, sanctions might be necessary for being non-responsive, missing deadlines, and failing to show up in court.

Some clients pick attorneys who match their energy—both the spouse and their attorney might be content to drag things out indefinitely.

This is the danger of the “friendly” separation, where everyone agrees to “just stay married on paper for now.” What seems like an easy, drama-free approach often becomes the most expensive mistake you can make.

What Happens to New Accounts Opened After Separation?

Here’s an important distinction: if you open a new brokerage account after separation, money deposited into that new account from post-separation earnings would be 100% your separate property.

The problem in our hypothetical was that the new account had maybe $10,000 in it. The bulk of the money—$400,000—remained in the original community property account.

If someone wanted to protect their post-separation investment gains, here’s what they should do:

- Immediately consult with an attorney about dividing the community property account

- Receive their share (like $200,000) as part of an early division of assets

- Deposit that money into a new, separate property account

- Build their separate property account with post-separation contributions and investment gains

Instead, by leaving $400,000 in a community property account and growing it to $900,000, someone would essentially be volunteering to build wealth for their ex-spouse.

The One Thing You Cannot Do

Here’s a critical warning: you cannot take money from a community property account and move it to a separate property account to “convert” it.

If someone took $400,000 from a community account and transferred it to a new account, that money would still be community property. The law calls this “tracing”—courts can trace where the money came from, and its character doesn’t change just because you moved it to a different account.

The only way to convert community property to separate property is through:

- A formal division of assets in your divorce

- A written agreement between spouses specifically transmuting the character of the property

- A court order changing the characterization

Moving money between accounts doesn’t accomplish any of these things.

The Strategy That Could Save Hundreds of Thousands

What should someone in this situation do? Here’s the winning strategy:

Option 1: Immediate Asset Division. File a motion for early division of community property assets. Argue that there’s no reason to wait years to divide investment accounts. Get a court order dividing the accounts now, even if other divorce issues remain pending.

Option 2: Written Agreement. Draft a formal written agreement with the ex-spouse stating: “From this point forward, each party’s investment accounts are their separate property. Each party bears sole responsibility for gains and losses. Neither party has any claim to the other’s post-separation investment growth.”

This agreement must be properly drafted and executed according to California law to be enforceable.

Option 3: Aggressive Case Timeline. Don’t let your spouse control the pace of divorce. If they’re dragging their feet, you push forward. File motions, set hearings, demand responses. Take control of the timeline.

Many people do none of these things. They wait years to even hire an attorney, then wait additional years while litigating.

Common Scenarios Where This Happens

This situation can occur in numerous contexts:

The Successful Business Owner: Someone owns a business valued at $500,000 at separation. Over five years of separation, they grow it to $2 million. Without proper division, they might have to share that $1.5 million growth.

The Real Estate Investor: Someone owns rental properties generating modest income at separation. Through active management and market appreciation, the portfolio doubles in value. The ex-spouse who contributed nothing could claim half.

The Stock Market Investor: Someone has a stock portfolio at separation and makes exceptional trades over the following years. Despite being separated, all gains could be community property.

The Cryptocurrency Holder: Someone owns crypto at separation that explodes in value. The ex-spouse who didn’t even know what cryptocurrency was could claim half the gains.

In each scenario, the spouse who created the value through their post-separation efforts faces losing half of it simply because they didn’t finalize the divorce quickly.

The Emotional Toll

Walking away from hundreds of thousands of dollars that you personally earned through your own skill and effort would be devastating for anyone.

Reaching a settlement and realizing you’re giving your ex-spouse half of the money you alone earned creates an understandable sense of injustice—that feeling of having worked so hard for something only to see half of it go to someone who contributed nothing to it.

But the law doesn’t care about fairness in this context. The law cares about property characterization and fiduciary duties.

Don’t Let This Happen to You

If you’re separated but not yet divorced, take these immediate steps:

Stop managing community property assets. If you have investment accounts, retirement accounts, or other assets that are community property, stop making discretionary decisions that could increase their value for your ex-spouse’s benefit.

Consult with experienced divorce attorneys immediately. Don’t wait years to get legal advice. The cost of consultation is nothing compared to the cost of delay.

Push for early asset division. File motions to divide assets now, even if other issues remain pending. The longer assets remain community property, the more risk you face.

Get written agreements about property characterization. If you and your spouse can agree on anything, agree in writing about which assets belong to whom going forward.

Document everything. Keep records of which accounts are community versus separate, where money comes from, and how assets grow.

Don’t trust informal arrangements. “We agreed you’d manage your accounts and I’d manage mine” means nothing legally. Get it in writing with proper legal language.

The Bottom Line

Time is literally money in divorce cases. Every month you delay is another month that community property assets can grow—growth that you’ll have to share even if you alone created it.

This is an expensive lesson that too many people learn the hard way. Don’t let the same thing happen to you.

Contact Ghazi Law Group at (818) 839-6644 or email contact@ghazilawgroup.com if you’re separated and have investment accounts, retirement funds, or other assets that are growing. We can help you develop a strategy to protect your post-separation earnings and avoid costly mistakes.

Don’t wait. The longer you delay, the more expensive your divorce becomes.